By Aspect Surveyors Limited · RICS-Regulated Chartered Surveyors

The UK commercial property market is in a classic “two-speed” phase: stabilising at the headline level, but with a widening gap between winning and losing assets. Offices and retail sit right at the centre of that divide. Below, we set out where things stand across both sectors, the core challenges facing asset owners, and five practical strategies for maximising returns in a difficult — but rich in opportunity — market.

1. Market Backdrop: Stabilisation After a Painful Repricing

After two years of rapid yield expansion, total returns for UK commercial property turned positive again in 2024, with retail leading the recovery and offices still lagging.[1]

By mid-2025, the picture looked broadly as follows:

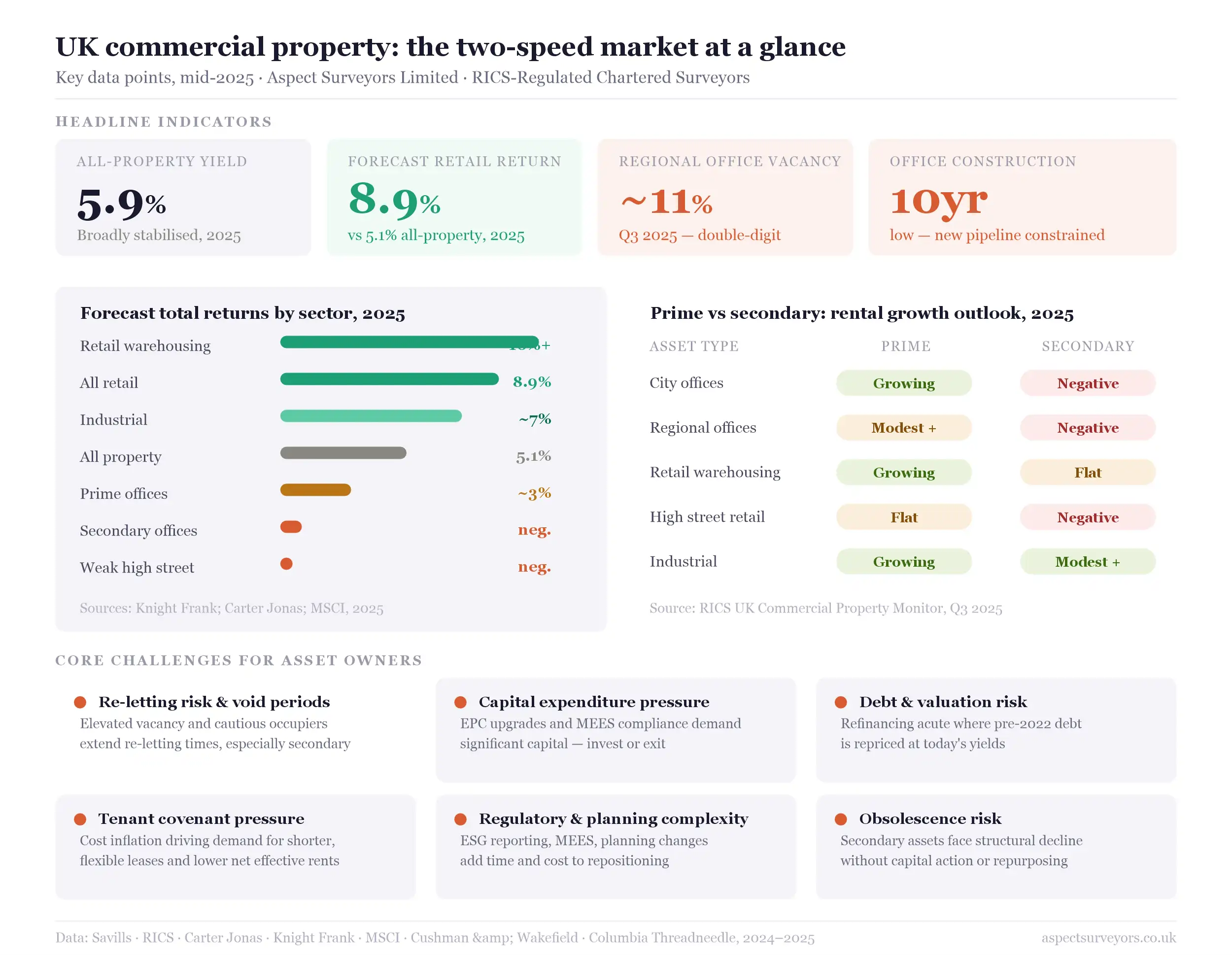

- All-property yields had broadly stabilised around 5.9%, with sentiment improving as investors looked ahead to potential interest rate cuts.[2]

- Industrial and retail were outperforming the all-property average in terms of capital growth, while offices remained in negative territory on a 12-month view, though performance was slowly improving.[3]

- Survey evidence confirmed that the polarisation between prime and secondary had become entrenched: prime office and industrial rents were still expected to grow modestly, while secondary office and retail faced flat or negative rental growth over the following 12 months.[4]

Against this backdrop, the story for office and retail assets is fundamentally about quality, location, ESG credentials, and flexibility.

2. UK Office Market: Flight to Quality and Stranded Secondary Stock

The office sector has undergone the sharpest structural shock of any major commercial asset class, driven by hybrid working, tightening ESG regulation, and elevated debt costs.

Key themes

Hybrid working is here to stay — but not in a way that eliminates the office. Businesses are rethinking space requirements and demanding more from the space they retain. The feared collapse in office-based employment has not materialised.[5]

Demand is heavily skewed towards Grade A, highly amenitised, sustainable space. Central London and major regional cores are seeing rental growth and strong competition for best-in-class offices, even as poorer stock struggles. The MSCI UK Quarterly Property Index shows rental growth concentrated in higher-quality assets, with weaker uplift in high-yielding, lower-quality properties.[6]

Vacancy rates remain elevated. Availability rose through 2024 in both the office and retail sectors. Regional office vacancy sat at around 11% in Q3 2025, despite some improvement in occupier take-up.[4][7]

New office construction is at a ten-year low. Developers have pulled back in response to uncertain demand, higher financing costs, and stricter environmental requirements. This is likely to constrain future prime supply and provide rental support for best-in-class buildings.[8]

The return to office is highly sector-specific. Manufacturers and consumer-facing businesses are tending towards more on-site working than B2B services firms, reinforcing the importance of understanding local occupational demand rather than relying on national averages.[9]

For office asset owners, this adds up to a stark reality: a smaller pool of tenants is chasing a smaller pool of high-quality space, while a large swathe of secondary offices risk structural obsolescence without significant capital investment.

3. UK Retail Property: Selective Strength and Repurposing

Retail has surprised many observers by emerging as one of the better-performing commercial sectors — albeit very unevenly.

Key dynamics

After substantial repricing, retail total returns have turned positive. Knight Frank projects all-retail returns of around 8.9% in 2025 versus 5.1% for the wider commercial property market, with retail warehousing and shopping centres expected to perform particularly well.[10]

There is a clear split between defensive and weaker formats. Retail warehousing, grocery-anchored schemes, and strong convenience pitches are holding up well, while weaker high streets — carrying too much secondary, low-productivity space — continue to struggle.

Structural headwinds persist. Online penetration, rising operating costs (wages, energy, business rates), and a fragile consumer environment are still driving store closures and Company Voluntary Arrangements in certain segments, particularly discretionary retail.

Repurposing is gathering pace. Legacy retail assets in urban locations are increasingly being converted into hotels, residential, and mixed-use schemes — reflecting both evolving planning policy and investor appetite for alternative uses on well-located sites.

Overall, retail is no longer the one-way bet it was before 2016, but nor is it the write-off some predicted during the depths of the pandemic. Income quality, tenant mix, and the potential for alternative use value are now the primary value drivers.

4. Core Challenges for Office and Retail Asset Owners

Across both sectors, asset owners typically face a broadly consistent set of pressures:

Re-letting risk and void periods

Elevated vacancy and cautious occupiers mean longer re-letting periods, greater incentive packages, and stronger competition — particularly for secondary stock.

Capital expenditure pressure

Upgrading EPC ratings, meeting tightening Minimum Energy Efficiency Standards (MEES), and delivering ESG-compliant, amenity-rich space demands significant capital. Owners must decide whether to invest or accept obsolescence and reposition or exit.

Debt and valuation risk

Higher interest rates, lower valuations, and tougher bank covenants are squeezing leveraged owners. Refinancing risk is especially acute where older debt was priced on pre-2022 yields.

Tenant covenant and affordability pressures

Retailers and office occupiers alike are navigating cost inflation and margin pressure, translating into a preference for flexibility, shorter leases, and sometimes lower net effective rents, especially in weaker locations.

Regulatory and planning complexity

ESG reporting obligations, health and safety requirements, accessibility standards, and shifting planning policies all add time and complexity to repositioning strategies — whether converting to residential, hotel, or mixed use.

5. Five Ways Asset Owners Can Maximise Returns

Despite these headwinds, well-considered strategies can materially improve income, reduce risk, and protect or grow capital values. Here are five practical recommendations.

Recommendation 1: Double Down on ESG-Led Repositioning of Viable Assets

For well-located office and retail assets, ESG-driven refurbishment is increasingly non-negotiable for owners who wish to preserve liquidity and maintain rental tone.

- Target a minimum EPC B (or better) on medium-term holds, anticipating tighter MEES requirements and institutional investor expectations.

- Prioritise works that reduce service charge and occupational costs: LED lighting, modern HVAC, smart metering, and upgraded building management systems.

- Enhance wellness and amenity offerings — natural light, cycle storage, shower facilities, quality common areas, and biophilic design — to align with occupier HR and ESG priorities.

- Obtain recognised certifications (BREEAM, NABERS, WELL, WiredScore) where viable to signal quality to institutional investors and occupiers alike.

This positions assets to capture the “green premium” in rents and yields, while materially reducing the risk of future obsolescence.

Recommendation 2: Reconfigure Space and Lease Structures for Flexibility

Occupier demand is now focused on flexibility, smaller footprints, and lower fit-out friction.

- Sub-divide larger floors into smaller, high-quality suites to appeal to a broader occupier base and reduce re-letting risk.

- Consider CAT A+ / plug-and-play solutions, where space is pre-fitted to a good standard so tenants can occupy quickly with minimal capital outlay of their own.

- In city-centre offices, explore a blend of traditional leases and flex or managed space — either self-operated or via partnerships with flex operators — to capture a wider occupier base and premium pricing for fully serviced, short-form accommodation.

- In retail, embrace shorter leases, turnover-linked rents, or stepped rents for the right covenants, aligning landlord and tenant incentives while preserving headline rental tone.

A more flexible product reduces voids, shortens letting periods, and often supports higher net effective rents across the cycle.

Recommendation 3: Sweat the Asset Through Proactive Management and Data

In a lower-growth environment, active asset management is the primary driver of outperformance.

- Invest in robust service charge and operating cost management: energy procurement, cleaning, security, and maintenance can all be meaningfully optimised. Lower total occupancy costs improve tenant retention.

- Use data and technology — from occupancy sensors to tenant engagement platforms — to understand space usage, tailor services, and build a community that occupiers value.

- Maintain a rolling lease events schedule to identify re-gear opportunities, break clauses, and expiries well in advance. Proactively approaching tenants with options that meet their evolving needs can enhance WAULT and income security.

- For retail schemes, curate the tenant mix continuously: blending essential retail, food and beverage, services, leisure, and community uses drives footfall and dwell time.

Well-managed assets with strong tenant relationships enjoy lower churn, higher occupancy, and more resilient income — all of which feed directly into valuation.

Recommendation 4: Explore Alternative Uses and Mixed-Use Potential

For secondary assets in good locations, the highest and best use may no longer be pure office or retail. Options worth exploring include:

- Residential conversion (private rented sector, build-to-rent, student, co-living) where planning and configuration allow, particularly for upper floors above retail.

- Hotels, aparthotels, or serviced apartments in locations with strong tourism or business travel demand, mirroring the trend of department stores and high-street assets being repurposed into hospitality or mixed-use projects.

- Health, education, or public sector uses — clinics, training centres, local authority hubs — which can offer long, secure income streams and strong social value credentials.

- Light industrial, urban logistics, or “dark store” concepts on edge-of-town or retail park locations, capturing the continued growth in last-mile fulfilment.

Early, realistic feasibility work — covering planning risk, structural constraints, and exit values — is critical. For genuinely secondary assets with limited occupational demand, unlocking alternative use value may be the most powerful route to protecting or enhancing returns.

Recommendation 5: Optimise Capital Structure and Recycle Out of Non-Core Stock

Returns are not only about the bricks and mortar: capital structure and portfolio strategy matter equally.

- Refinance or reshape debt where possible to reduce interest costs, extend maturities, and de-risk covenant breaches — even if it means accepting a modestly higher margin in exchange for greater certainty.

- Dispose of non-core or sub-scale assets where capex demands are high and long-term viability is questionable. Recycling capital into stronger, future-proofed assets — or paying down debt — can materially improve risk-adjusted returns.

- Explore joint-venture or forward-funding structures with capital partners who bring both appetite and expertise for development or heavy refurbishment, rather than stretching balance sheets.

- Align hold/sell decisions with clear business plans and IRR hurdles, rather than waiting for a cyclical uplift to rescue underperforming stock.

Being decisive about where to deploy capital — and where not to — is one of the few levers asset owners fully control in an uncertain market.

Conclusion

The current UK commercial property market is neither booming nor collapsing: it is sorting winners from losers more ruthlessly than at any point in recent memory.

For office and retail asset owners, the coming years will reward a clear-eyed view of asset quality and long-term relevance; a willingness to invest in ESG credentials and tenant experience where the location justifies it; flexibility in product, leasing, and tenant mix; creativity around alternative uses; and disciplined, opportunistic capital allocation.

Those who act early and thoughtfully can still generate attractive returns, even in a challenging environment. Those who delay risk watching their assets slide into structural obsolescence.

Aspect Surveyors Limited is a RICS-regulated chartered surveying practice. If you would like to discuss any of the themes raised in this article in relation to your own portfolio, please get in touch with our team.

Sources

| # | Source | Publication | Date | URL |

|---|---|---|---|---|

| [1] | Columbia Threadneedle Investments | UK Commercial Property Returns | 2024 | columbiathreadneedle.com |

| [2] | Savills | UK Commercial Property Market in Minutes | 2025 | savills.co.uk |

| [3] | Carter Jonas | Commercial Property Market Update | 2025 | carterjonas.co.uk |

| [4] | RICS | UK Commercial Property Monitor | Q3 2025 | rics.org |

| [5] | Buckles Law | Hybrid Working and the Office Market | 2025 | buckles-law.co.uk |

| [6] | MSCI | UK Quarterly Property Index | 2025 | msci.com |

| [7] | Cushman & Wakefield | UK Office Market Statistics | Q3 2025 | cushmanwakefield.com |

| [8] | Financial Times | UK Office Construction Pipeline | 2025 | ft.com |

| [9] | British Chambers of Commerce | Workplace Trends Survey | 2025 | britishchambers.org.uk |

| [10] | Knight Frank | UK Retail Property Outlook | 2025 | knightfrank.co.uk |